Investing Basics

How a rewards card can fund startup investing

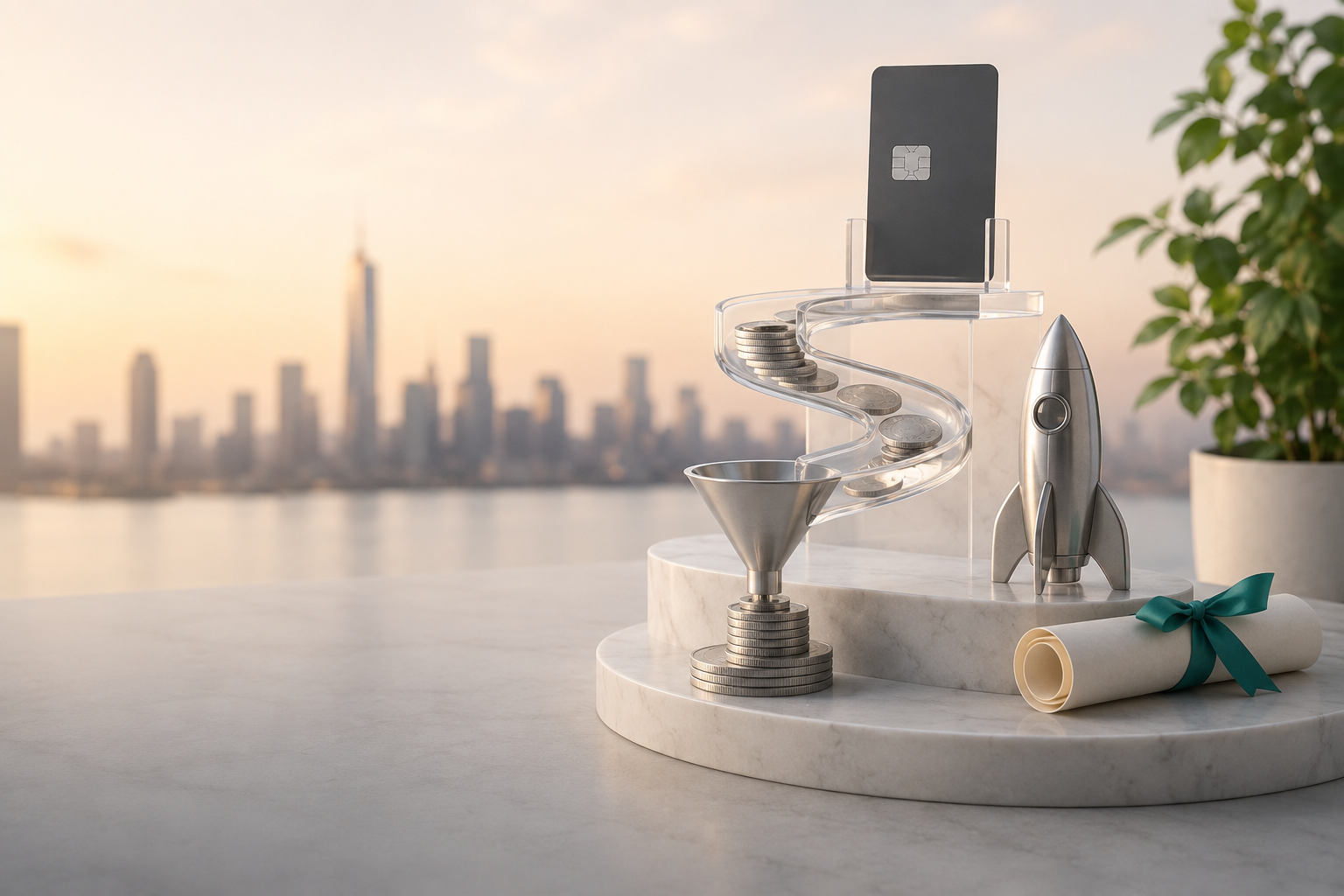

A rewards card can fund startup investing when its rewards are routed into startup equity instead of points or cash back. Here is the full chain, and the risks.

Key takeaways

- A rewards card funds startup investing when the cash value of its rewards is routed into startup equity instead of returned as points, miles, or a statement credit.

- The chain has three links: interchange-funded rewards on everyday spending, a deposit into an investing account rather than a redemption, and a purchase of startup shares through Regulation Crowdfunding.

- Regulation Crowdfunding, adopted by the SEC under the JOBS Act, is what lets non-accredited investors buy into startups; in March 2021 the SEC raised the per-company annual cap to $5 million.

- Because rewards from normal spending are small, the per-investor Reg CF limits rarely bind, and the dollars invested are money you were not otherwise going to invest.

- The risk is high: about half of new U.S. businesses close within five years (Bureau of Labor Statistics), startup equity is illiquid, and money allocated to a failed startup can go to zero.

A rewards card can fund startup investing when the cash value of its rewards is routed into startup equity instead of coming back as points, miles, or a statement credit. The chain is simple: the card earns rewards on everyday spending, those rewards are deposited into an investing account rather than redeemed, and the money buys shares in early-stage companies through Regulation Crowdfunding, the SEC rules that let almost anyone invest in startups. No new spending, no separate deposit. The reward itself becomes the investment.

This is the mechanism behind cashback-to-equity, and it is one of several ways to invest credit card rewards. What follows is how the chain actually works, link by link.

How a rewards card turns spending into startup ownership

Step 1: the card earns rewards on everyday spending

Every time you use a credit card, the merchant's bank pays the card's issuer a small interchange fee, usually a few percent of the purchase. That fee is where rewards come from: the issuer hands part of it back to you as cash back, points, or miles. A rewards card is really just a system for returning a slice of interchange to the cardholder. Nothing about that slice has to come back as spending power.

Step 2: the rewards are routed to an investing account, not a statement credit

The pivot is where the reward goes. Most cards send it back as a statement credit or points, which pull you toward more spending. A card built for investing instead deposits the cash value into an investing account. Some cards already do this with public-market brokerage accounts. A cashback-to-equity card points that same flow at private markets.

Step 3: the money buys startup equity through Regulation Crowdfunding

Once the reward is sitting as money in an investing account, it can buy an asset. For startup investing, that asset is shares in an early-stage company, purchased through Regulation Crowdfunding (Reg CF). Reg CF is the legal on-ramp that makes the whole chain possible for ordinary spenders, which is worth a closer look.

Why Regulation Crowdfunding makes this possible

Before 2016, investing in a private startup was mostly limited to accredited investors, people who clear high income or net-worth thresholds. Regulation Crowdfunding changed that. Adopted by the SEC under the JOBS Act, Reg CF lets companies raise money from the general public, and it lets non-accredited investors buy in. In March 2021 the SEC raised the amount a company can raise this way to $5 million per year (up from $1.07 million), which widened the pool of deals an everyday investor can reach. You can read the SEC's overview on Investor.gov.

Reg CF also caps how much each person can invest over a 12-month period, based on income and net worth, so the amounts stay proportionate to what someone can afford to lose. The current limits are set out by the SEC on its Regulation Crowdfunding page. For a rewards-funded approach, those caps rarely bind, because the rewards from normal spending are small relative to the limits.

The math: small rewards, real ownership

The appeal is that the dollars are ones you were not going to invest anyway. Put $2,000 a month of ordinary spending on a card paying a few percent back, and the rewards add up to a few hundred dollars a year. Routed into a statement credit, that is a small discount you spend again. Routed into startup equity, it is a few hundred dollars of ownership you hold, accumulated without changing how you spend.

That is the upside framed honestly: the money is found money, and turning it into ownership costs you nothing extra. The trade is that the value is no longer fixed. (Illustrative figures, not a forecast or a promise of any return.)

The risks of funding startup investing with rewards

This routes rewards into one of the highest-risk asset classes there is, so the risks are real and worth stating plainly.

- Early-stage companies fail at high rates. About half of new U.S. businesses close within five years, according to the Bureau of Labor Statistics, and early-stage startups, the kind Reg CF funds, fail at even higher rates. Money allocated to a startup that fails can go to zero.

- The shares are illiquid. Private startup equity usually cannot be sold on demand. There is often no market for years, if ever, so this is money you should expect to lock up for the long term.

- The value is no longer fixed. A statement credit is worth a dollar today and a dollar next year. A startup share is worth whatever someone will pay later, which may be more, less, or nothing.

None of this is an argument against the model. It is the case for understanding exactly what you are holding, and for only routing rewards you can afford to put fully at risk.

Where EarlyBird fits

EarlyBird is building a cashback-to-equity credit card. When the EarlyBird Card launches, the rewards you earn from everyday spending will be allocated by a federally covered, Series 65 investment adviser into a curated set of early-stage offerings, so the full chain above runs automatically instead of by hand.

The card and the investing service are not live yet. For now, the way to take part is to join the waitlist.

Frequently asked questions

How can a credit card fund startup investing?

By routing the cash value of its rewards into startup equity instead of returning it as points, miles, or a statement credit. The card earns rewards on everyday spending, those rewards are deposited into an investing account rather than redeemed, and the money buys shares in early-stage companies through Regulation Crowdfunding. The reward itself becomes the investment, with no new spending and no separate deposit.Where do credit card rewards actually come from?

When you use a credit card, the merchant's bank pays the card issuer a small interchange fee, usually a few percent of the purchase. The issuer returns part of that fee to you as cash back, points, or miles. A rewards card is essentially a system for handing a slice of interchange back to the cardholder, and that slice can be routed into an investing account instead of being spent.Do you have to be an accredited investor to invest rewards in startups?

No. Regulation Crowdfunding (Reg CF), adopted by the SEC under the JOBS Act, lets non-accredited investors, not just high-income or high-net-worth individuals, invest in early-stage companies. Reg CF sets per-investor limits over a 12-month period based on income and net worth, but because rewards from ordinary spending are small, those caps rarely come into play.How much can rewards realistically add up to for startup investing?

It depends on your spending and the rewards rate. As an illustration, $2,000 a month of spending on a card paying a few percent back generates a few hundred dollars of rewards a year. Routed into startup equity, that is a few hundred dollars of ownership accumulated without changing how you spend. These are illustrative figures, not a forecast, and the value of any startup investment can rise or fall to zero.Is funding startup investing with credit card rewards risky?

Yes. Startup equity is one of the highest-risk asset classes there is. About half of new U.S. businesses close within five years according to the Bureau of Labor Statistics, and early-stage startups fail at even higher rates, so money allocated to a failed company can go to zero. The shares are also illiquid and may be impossible to sell for years. Only rewards you can afford to put fully at risk should be routed this way.

Comrie Flinn · Founder & CEO

Comrie founded EarlyBird after building an SEC/FINRA-licensed funding portal earlier in his career. He writes about consumer fintech, private-markets access, and what it takes to make compliance feel like a feature.

Read more from Comrie FlinnA credit card that turns rewards into ownership of curated private assets.

Join the waitlist to be among the first cardholders.

Join waitlist